By Jeremy Horpedahl, Ph.D.

By Jeremy Horpedahl, Ph.D.

Jeremy Horpedahl, Ph.D.

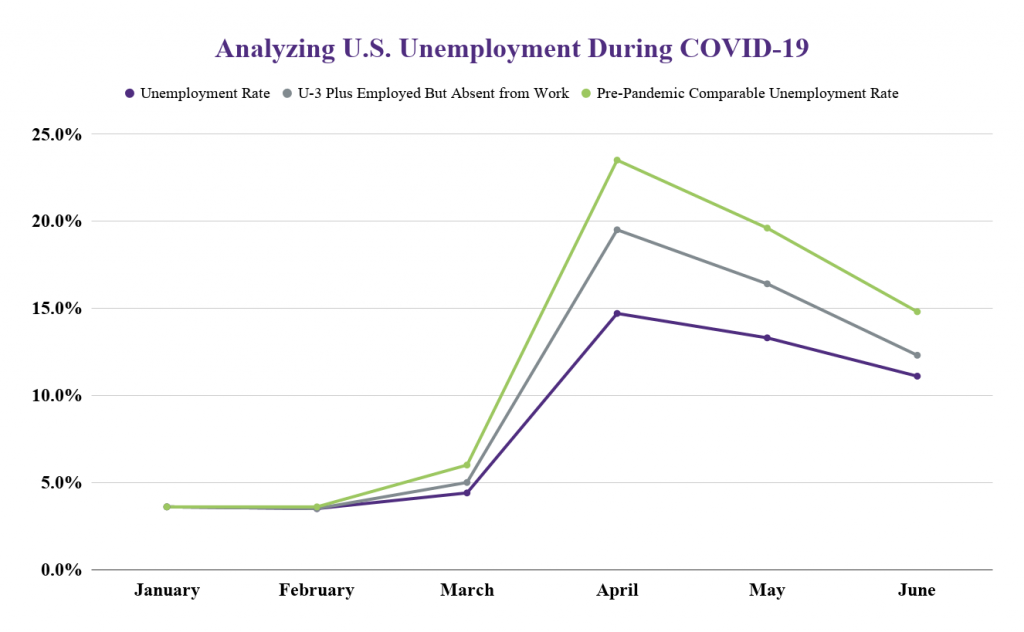

We all know that we are going through one of the worst economic downturns in US history. But how bad exactly is the downturn? The recently released Gross Domestic Product data for the second quarter of 2020 paint a very grim picture, with the headline number suggesting that the economy contracted by -32.9%.

GDP is a measure of all economic activity that takes place in a quarter or a year. Was there really one-third less activity in the second quarter compared with the first quarter? No there was not. The actual number is about a 7% decline. I’ll explain more how I came up with that number, but let me stress this is still a very bad number. It’s the worst we have on record, possibly the worst in US history, probably even worse than any one quarter of the Great Depression (if we had directly comparable data). Still, a number like -32.9% is not a very helpful number in the current context.

Interpreting economic data is challenging during the current economic crisis. My intent is not to downplay the harm, but to give it proper context. For example, I have previously written that the unemployment rate understates how much pain there is in the labor market right now. In contrast, the recently released GDP data overstate the economic pain.

Read more at Texas CEO Magazine.

Horpedahl also recently appeared on The Cato Institute’s Daily Podcast to give a quick rundown of the numbers. Listen here or anywhere you get podcasts.

Japan is one of the world’s most advanced and largest economies, yet lags behind in its use of e-payment and e-commerce.

Japan is one of the world’s most advanced and largest economies, yet lags behind in its use of e-payment and e-commerce. Cynthia Burleson, director of the Center for Insurance & Risk Management in the UCA College of Business, was featured in June on an episode of the Insurance Town podcast.

Cynthia Burleson, director of the Center for Insurance & Risk Management in the UCA College of Business, was featured in June on an episode of the Insurance Town podcast.

Hannah Robinson, a senior

Hannah Robinson, a senior